Underlying much of the efforts of national and local authorities to regulate commerce were two fundamental issues. First and foremost the maintenance of the 'just' price in commercial exchanges – and, by association, the just wage, which was seen as, in essence, the price for labour. For exchange, whether of goods or services, was understood as a foundation-stone of society, part of the glue that motivated people to associate with each other and form communities. It was both morally virtuous, or 'just', and pragmatically sound (in terms of preserving social harmony) to ensure that there was fair play to both parties in commercial transactions. Secondly, the taxation of commerce increasingly became an important source of seigneurial revenue, and particularly revenue due the Crown; the latter was justifiable not simply because the king was the ultimate lord of the realm, but also because it contributed funding that enabled administration of the state, protection of the interests of its people, and preservation of peace and security – all preconditions for honest commerce to flourish.

In any exchange the challenge is how to attain equality of value in the different things parties are exchanging. To some extent this is governed by the particular needs of the parties, which themselves may not be consistent from occasion to occasion, and is left to a bartering process. A more objective approach is to have standards by which exchange items (again, whether goods or services) can be evaluated in common terms. Money is a key intermediating tool for measuring value – something that requires the intrinsic value of coins to remain valid and reliable over time. Monetary values could then be accurately assigned to units of commodities or labour. But also necessary to assigning monetary value to goods were standardized weights and measures that enabled determination, in a fair and reliable manner, of the quantity or size of units being exchanged.

An exhibit in Colchester Castle Museum includes (at top)

a set of stacked lead weights of ca.1500 discovered in the borough, and (at bottom)

spherical steelyard weights

with bronze casing filled with lead or clay.

Photo © S. Alsford

Used in conjunction these tools of standardization could permit national and local authorities to engage in a certain degree of price-setting. The most determined effort to enforce this was in regard to the most basic needs of the populace: food and drink; the Assizes of Bread and Ale used mathematical formulae related to prices of raw materials (which themselves were recognized as fluctuating based on supply and demand) to establish set prices seasonally for specified units of those key dietary components, also taking into account that there were different qualities of products which warranted small variations in price. That the periodic judicial sessions through which these assizes were administered seem consistently to have fined, almost as a matter of course, large numbers of producers for infringements suggests either that the set prices could not be enforced effectively or that local authorities appreciated that market realities were always a factor in price determination and that assize prices were more in the nature of a guideline, beyond which any profit was taxable, and excessive profit – whether obtained by meddling with prices, with the unit size, or with the weights and measures used to evaluate unit size – punishable.

Price-setting would hardly have been practicable, on a daily, or even a market session by session, basis, for the wide range of goods available in the marketplace. Although bread, ale, wine, fish and cloth, as essential and heavily traded items, could be regulated to some extent in terms of prices and/or unit sizes, the 'just price' for many goods must have been considered the effective market price at any given point in time; that is, some balance point between what sellers thought it reasonable to ask and buyers were prepared to pay. This took into account factors such as local supply and demand and the value of the labour, expenses, or even risk of the seller in producing or transporting goods (this value being considered by theorists the extent of a valid profit margin and related, once more, to efforts to set and control wages). The market price emerged from a process of bargaining, in which buyer and seller – while in principle they might be expected to operate within reason so that the needs of each (on the one hand sufficient profit to make a living, on the other affordability of necessaries) were respected – were in practice at liberty to use their wits and even deceit to gain an advantage over the other; Caxton recounts a hypothetical example of a civilized negotiation in which both parties end up satisfied.

The concept of a fluctuating market price was recognized in the Middle Ages, understood not as whatever was being demanded by an individual seller, which might be excessive rather than just, or as what any individual purchaser ended up paying, but as something that emerged from a common consensus of market users through a series of completed transactions satisfactory to both parties. Were any effort made by the authorities to identify a fair price for a given product, it would have had to take into account knowledge of prior trading sessions and current changes in availability of, or public need for, the product; such knowledge should have been obtainable by borough executive officers from market supervisors, or even through the aggregated experiences of the town councillors, who were buyers and/or sellers in the marketplace. It is not clear from surviving records, however, that any such effort was routinely made; but a sense obtained from the market of what a fair price should be may have helped alert authorities to possible attempts to subvert the natural flow of market processes in order to charge unjust prices.

Kings were more prone to price intervention, but this was generally prompted by specific crises, or perceived crises, such as when Edward I's installation of his war-time administration at York increased demand for victuals there, pushing prices up, and angering the king who introduced regulations that included price controls; or in later periods, when famine or plague pushed prices to alarming levels. There are certainly instances of civic authorities issuing ordinances that set prices for certain commodities; but again, we may suspect these were responses to specific problems that had arisen and that prices set reflected what was believed to have been commonly paid for the commodities in normal times, perhaps with some allowance for a shift in the supply/demand balance, but more likely with the aim of holding the line. There seems to be no evidence of regular, systematic price-setting beyond the administration of the assizes; for which, in the case of ale, at least some towns appointed ale-conners to check, during the intervals between judicial sessions, on the quality of each new brew and the price being demanded per gallon, as well as keep an eye on the measures used by brewers and retailers of ale.

Reliance on the market to establish reasonable prices for most commodities does not mean that the authorities took a laissez faire approach to the marketplace. Even where it was not feasible to set fair prices, qualities of products could be monitored. The grouping together, within marketplaces, of dealers in particular kinds of products was probably aimed at facilitating supervision of prices, unit sizes, and product availability and quality; the elusive market wardens, or other borough officials, could more easily get a sense of current prices for and quality of a particular product, to help in determining whether sellers operating outside the marketplace were charging exorbitant prices or offering substandard goods. Authorities were not fond of traders operating outside of the marketplace or market hours because of the difficulties this caused for supervision and for identifying fraud.

The oldest surviving liquid measure of an ale gallon, of a copper alloy, made and sealed

at the Royal Mint (Tower of London) 1653, for the use of the city of Exeter; collection

of the Royal Albert Memorial Museum, Exeter.

Photo © S. Alsford

Certain aspects of trading, governing fair prices, were more open to policing.

Shops might be visited either on a systematic basis or by spot-checks to ascertain

product qualities and prices, or to examine shopkeepers' weights or measures,

to assure that they complied with standards – at

Norwich such inspections had to be made

several times a year, whereas at Ipswich

the regularity seems to have been left to the discretion of the bailiffs; the requirement

that private weights and measures had to receive a stamp of official approval before

they could be used was a natural corollary of this aspect of regulation.

The Assize of Measures issued by Edward I (ca.1303) had given more precise

specification, basing weight standards on a sterling penny weighing 32 grains of corn:

Standard weights and measures produced 1826 for the Corporation

of Winchelsea and now in the Court Hall Museum there. (above) Brass weights. (below)

Measures of capacity: bushel, half bushel, quarter bushel.

Photos © S. Alsford

With clearer knowledge of standards, and authoritative models in hand for comparative purposes – in the reign of Edward II it was decided to make brass reproductions of the official ell and bushel and distribute them to towns across England – not only private weights and measures but goods offered for sale could be examined in terms of conformity with standards as well as other qualities. In some cases traders might be required to come periodically, with samples of their merchandize, to some central location for interrogation and inspection. At Lynn traders were required to bring their weights and measures to the annual leet court sessions for checking, so that those that were inaccurate or unsealed could be identified, and those who neglected to do so would be fined; from these proceedings we learn that, in the 1360s, the more prosperous traders owned a good set of weights – typically a half hundredweight, 1 quarter, 1 stone,8 pounds, 4 pounds, 2 pounds, 1 pound, and a half-pound, although dealers in metal had heavier weights. Measuring sticks – ells and virgas – also seem to have been fairly common.

Stern action had to be taken against those who used ploys to try to manipulate market prices, such as by monopolizing or hoarding goods to create artificial scarcities, or by conspiracy or intimidation aimed at forcing prices up. Part of the reason forestalling and regrating were frowned on was because they introduced an additional profit-taker into the marketing process without adding anything to the value of the product, thus pushing the selling price into 'unjust' territory. There was inevitably a high degree of reliance on public complaints to draw attention to alleged offenders.

Standard weights and measures produced at London, 1824,

to Exchequer specifications, for the Borough of Tewkesbury. (above) Three graduated

brass weights, spherical with loop handles. (below) Set of graduated brass measures

of capacity. Now in the borough museum.

Photos © S. Alsford

The taxation of commerce has been addressed elsewhere, and noted as, from the perspective of merchants, one of the costs of doing business – a cost that a minority sought to evade through smuggling (or at least only a minority were so accused). Here we may add a little something more on that process of taxation from the perspective of the merchant who paid it. At the local level of commerce market regulations and controls limited, to some extent, profit-taking, though countered that drawback by creating a more level playing-field, in which unfair competition was reduced by imposing additional costs on competitors who infringed regulations or failed to comply with standards. Such costs might take a variety of forms: fines adjusted to the severity or regularity of the offence; confiscation or destruction of merchandize; public shaming of such offenders, with any consequent damage to reputation; and in extreme or persistent cases, temporary or permanent deprivation of occupation or trading privileges.

However, in the sphere of international commerce – whether importing/exporting, or simply wholesale trading with visiting foreign merchants – although traders might still be under some societal expectation of behaving virtuously, through fair and reasonable negotiations, they were in practice at liberty to strike whatever deal they could, without direct official supervision, price controls, or other limits on the amount of profit they might earn (except in special cases where an aggrieved party to a deal later alleged a significant discrepancy in price and value of goods). Profitability of wholesale, long-distance commerce lay, after all, partly in cumulative market knowledge and personal enterprise in finding goods where they could be bought cheaper then taking them to wherever demand allowed them to be sold dearer, usually at enhanced risk to the trader. In return for the greater freedom of action in this type of commerce – limited only by the requirements that common standards of weights and measures would be applied, and that any deals reached (if documented or witnessed) would have the force of legal contract backed up by the king's courts and, if necessary, by international diplomacy – costs were imposed in the form of royal surcharges, notably customs duties; while such costs existed, as tolls, at local levels too, they were generally more moderate and not applicable to large categories of traders.

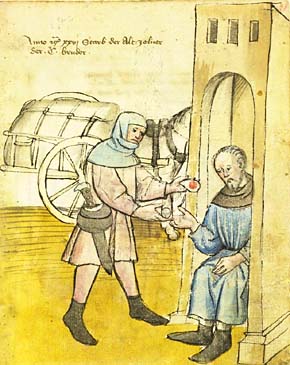

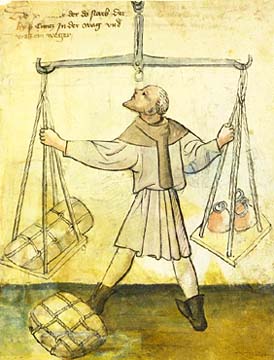

The collection of tolls and customs provided employment for a large cadre of collectors

and lesser-known officials. (above) Posthumous portrait (1426) of an unnamed toll collector

depicted sitting in a booth by the road; he is receiving a coin from a carter who

is transporting a bale of goods in a two-wheeled cart, and has in return issued the carter

with a sealed chit that confirms toll has been paid. This is a collector of local tolls,

chargable on the cartload rather than on a specific weight of goods.

(below) a weigher of customable

merchandize, probably operating at the port.

From the Hausbuch der Mendelschen Zw�lfbrüderstiftung

Surcharges on commercial activity typically began with costs such as (in different cases) stallage, scavage, quayage, lastage, cranage, tronage, mensurage, and aulnage; these might be payable directly to the king or to private landlords as part of their territorial rights or through grant from the king. They were part fees for services and part licensing of privileges, whereas customs proper were essentially taxes. Although it is not entirely clear, it appears that the various charges, if applicable, were payable to different officials at different locations, some at the point of arrival (whether town bundary or quayside), some around the marketplace; navigating through the various payment processes – a rigmarole repeated in some form at each stop-over during a mercantile voyage – must have been time-consuming for merchants.

Charges such as mensurage, pesage, tronage, and aulnage were a necessary pre-requisite to assessment of tolls or customs, by measuring the goods being imported or exported. At Lynn, where some port tolls, collected by the bailiffs of the Tolbooth, were shared between the Bishop of Norwich and the Earl of Arundel, the former's take in 1236/37 from tronage alone was 60s., while in 1335/36 the bailiff representing the king (who had temporarily acquired what seems to have been a one-eighth share) accounted for 6s.4d. from tronage and 8s.10d. from mensurage; total revenues from the Tolbooth jurisdiction netted the king £6 5s. 9¾d. in 1338/39 – not a huge amount, particularly after expenses were paid, but the king had innumerable such small revenues. On the other hand, cranage, plankage, and quayage were in the hands of Lynn's merchant gild, earning it £14 8s.10d. in 1385/86, most of which derived from fees for use of the crane. Once the type, quality, quantity, size, and/or weight of each batch of mercantile goods had been ascertained, the appropriate customs and subsidies payments could be calculated. Upon paying, or providing some guarantee of payment, the merchant would be issued with some kind of receipt and the batches of goods themselves would be marked to identify what they contained and when/where they had passed through the customs process.

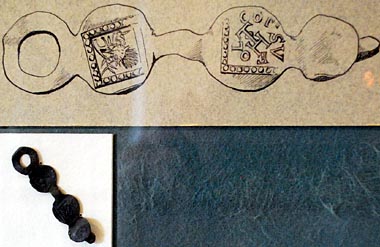

(above) A walrus-ivory seal of mid-twelfth century found at York; the inscription

identifies it as belonging to Snarrus the toll collector (whose name points to

Scandinavian ancestry). He is depicted on the seal as dropping three coins into

a purse held at the end of his outstretched arm. The seal, which has a pierced appendage

at top (indicating it may have been worn around the neck like a pendant) was likely

used for authenticating receipts of toll payments. That a toll collector owned such

a seal suggests he had long-term tenure of the office, or perhaps was farming it; it

was helpful for the seal to identify the official in case there were queries later.

(below) Fourteenth century silver seal applied to customs documents issued at the

Westminster wool staple; the seal shows four woolsacks and the keys of St. Peter.

Replica of an original in the British Museum.

Photos © S. Alsford

The growth of the English cloth-making industry meant that increasing attention had to be given to quality control of, and collection of duties on, cloth destined for export. It was checked, potentially at various stages, for quality and for adherence to statutory sizes by searchers of associated gilds – where they existed – and by county officials called aulnagers (or alnagers, their name deriving from the Latin ulna, meaning ell), appointed by the Crown. The aulnager collected the subsidy (4d. per entire broadcloth in 1353, over and above any import/export customs due) payable by the seller of cloths – whether weaver, cloth-finisher, or merchant – along with a fee for his services. Fairly large numbers have survived (particularly from London and mostly post-medieval) of the lead seals aulnagers applied to bales of cloth, to show that they had been inspected and the tax due had been paid. Imported cloth was also subject to such inspection and sealing.

Aulnager's seals from the collection of the Museum of London.

(above) Fifteenth and sixteenth century seals.

(below) A seventeenth century seal recovered from a wreck off the coast of Norway,

with drawing (produced for an exhibit in the Corpus Christi Guildhall, Lavenham),

to show the markings on the seal; such markings came to signify the type of cloth,

its size and place of origin, and identification of the aulnager or the cloth-maker.

Photos © S. Alsford

The aulnage regulation initially applied mainly to woollen broadcloths, the most commonly produced size of cloth, but gradually extended to other types of cloth; lower quality textiles intended to clothe poor people and those (called the 'new draperies') whose manufacture was a specialty of some particular locality, were not included until the sixteenth century, when thickness or weight of cloths also became more of a concern for aulnagers. But regulation of the width of cloths can be traced back to the Assize of Measures (1196), and the first known effort to standardize lengths was in 1278; the following year royal officials were appointed to assure conformity of the sizes of cloths being sold at English fairs and markets, although we do not hear of the title 'aulnager' until 1315. Substandard cloths were confiscated and probably destroyed.

Aulnagers are known to have been marking approved cloths by 1328, though in what manner is uncertain. The administration of the assize of cloth proving a disincentive to the import of foreign cloths, often produced to other standards than those of England, the statute of 1353 specified that instead of requiring cloths be particular sizes and having non-compliant cloths subject to forfeiture, aulnagers should mark the cloths to indicate their actual size and adjust the subsidy accordingly; the aulnager's fee was limited to a halfpenny for each cloth of the statutory size, a farthing for cloths up to fifty percent smaller, and nothing for cloths even smaller. The aulnager was to apply his seal to every inspected cloth, or package of cloths, which could not be sold unless the seal was affixed. Lead was being used for such seals from the late fourteenth century; lack of survival of earlier examples (although some seal matrices have survived) may suggest a more perishable material, such as wax, was used initially [Geoffrey Egan, Provenanced leaden cloth seals, Ph.D thesis, University of London, 1987, p.18]. A statute of 1389/90 required cloth manufacturers also to apply their marks to their products.

The post of aulnager was one sought by many career administrators, and must have offered scope for corruption; some of the accounts they drew up have been shown to be highly inaccurate. As cloth manufacturing grew, policing of quality became increasingly impracticable or less effective.